-

The Nvidia Bear Case

NVDA is kind of in a no-man’s land in terms of sentiment and price action, bouncing in a tight range for months and some mix of bullishness and skepticism depending on who you ask. Here I figured I’d put out the bear case which I’m starting to warm up to.

Recently Meta stock has been in a significant downtrend. The last time Meta was spending wildly while the stock collapsed was during the development of the metaverse, which they had hired tens of thousands of employees to support. When pressure mounted from prominent shareholders, Zuckerberg did an about face and essentially shut down development. If the selling continues, I do believe there will be a reckoning and pressure will mount for Zuckerberg to show return on investment. This is not new, as recently Meta has turned up the profit spigot by showing more ads which was a clear effort to justify the AI investment. But now the stock is sliding again. Eventually if the stock of Meta and other hyperscalers falls enough I believe they will be required to cut spending which would be hugely negative for Nvidia. Keep in mind it wouldn’t necessarily have to be a 180, but rather just a reduction in spending.

Another issue is the foundation model companies like OpenAI and Anthropic. Both companies have reported massively growing ARR, but I believe much if not the vast majority of this revenue is coming from enterprise software companies that have incorporated these services into their products and have decided to eat the cost up front. It’s not clear that there will be increased purchases to offset these costs. Here again, I don’t think it’s going to be long before these companies reduce AI spend as the prices collapse. That is sort of a second derivative to NVDA, but if OpenAI suddenly sees a drop in revenue, they will become even more cash-strapped.

Finally, although I don’t like to throw stones, in the past few days I’ve noticed that certain personalities who enjoyed massive success on the podcast circuit over the past couple of years are hugely bullish all of a sudden. It sounds dickish and a stupid reason to be short but I do believe nobody succeeds forever and individual investors go through cycles like everything. As Bruce Kovner said, there are a lot of one hit wonders in the stock market.

-

Thoughts at the quarter mark

Back in my January post where I made my predictions for 2026, I mentioned the idea of distortions being created by extended periods of high liquidity and little lasting volatility. I believed and still do that we are late cycle and when you get late in a cycle ideas that are plainly untrue not only are believed to be true but are actually calcified into universally accepted truths. So by the time you are late in the cycle things that should be considered major potential risks to the market and economy are still believed to be buying opportunities.

Recently there has been a major upheaval in energy markets and oil has surged to around $100 a barrel as I write this. I think that this is a major issue for markets and one that as much press as it’s received is not really being taken all that seriously by most people or believed to be all that serious.

Many people don’t seem to realize how insanely well things have lined up over the past several years to enable the situation we are in now, where the S&P has gone up sixfold since the GFC.

You’ve had two events that resulted in unprecedented liquidity creation through stimulus and zero rates. Another part of the story that hasn’t gotten as much attention, or perhaps has been taken for granted, has been the shale revolution and the incredibly low price of oil and gasoline throughout this run. We as a society have taken $2.50 gas as the standard despite the cost of nearly everything else going up. Fuel simply hasn’t kept pace because the United States has maxxed out its own oil production and, this is key, actively drained the strategic petroleum reserve. This occured first under Biden due to a short term spike in gas prices and the government never re-upped the supply. We’ve been running everything hot but when you do that for too long, it becomes accepted as the norm.

I don’t think there is any part of the economy that will be untouched by higher oil prices. I talked about oil being a major potential risk to the ride-sharing and food delivery apps like Uber and I think those are great areas to short given the resolve of the investor base and unending bullishness. But there are many others.

The hyperscalers for example have been given enormous leeway to bet on AI and spend all of their FCF on chips. But what happens if that suddenly changes? What if interest rates rise and cash becomes more scarce? Even just a little wobble will likely make a huge difference in what the market chooses to reward. I do think it’s a bit telling that recently stocks that are betting on software, automation (essentially the opposite story as software), hyperscalers and chip companies have all been performing varying degrees of not great. What this seems to be suggesting is that suddenly the market is implying that AI won’t be an immediate tailwind to any sector.

Why? Well because software could benefit from AI but starting last year was assumed to be getting killed off by coding assistants at which point automation stocks soared but now those too have stalled out. NVDA has been in a flat trend for months and yawned at the latest announcement at GPC that revenues were projected to double to over a trillion. Hyperscalers who are spending all the money on chips also have been performing poorly. If one were to assume a ROIC even approaching what NVDA and the hyperscalers have been hyping those stocks should be going up along with earnings estimates. But they aren’t. The fact that not one previously-annointed beneficiary sector is performing well could well be an early warning sign about this trade that has provided a massive tailwind to the S&P over the past three years.

The market has had pretty bad breadth recently too with the VALUG solidly in a downtrend and on a sell signal. I can’t see a reason to like US equities here and think we have a lot of pain left in time and price ahead.

A last word on distortions

I’ve noticed lots of distortions today that I don’t think have a parallel- an enormous number of people heralded as geniuses, way out of proportion with historic percentages, mediocrity in the workforce being accepted because AI masks deficiencies because companies for now are no longer focused on technical excellence but rather leveraging AI. One in particular is that things that are genuinely useful on a small scale are believed to be many multiples of useful and are predicted to have outsized impact on the world. In other words, mountains are made out of mole hills. I’m obviously referring to AI here.

While AI chatbots and agents are cool and definitely useful, I do believe that their projected impact in the near term has been blown way out of proportion. I use multiple AI tools a day. I’d say it’s allowed me to learn new skills at hyperspeed. That’s amazing. But it hasn’t resulted in an enormous increase in concrete output in my view. Rather its enabled me to become surface level competent in a much wider array of areas. I am still in the camp that this trade is going to reverse because the tools just aren’t there.

-

Automation is coming for our jobs once again

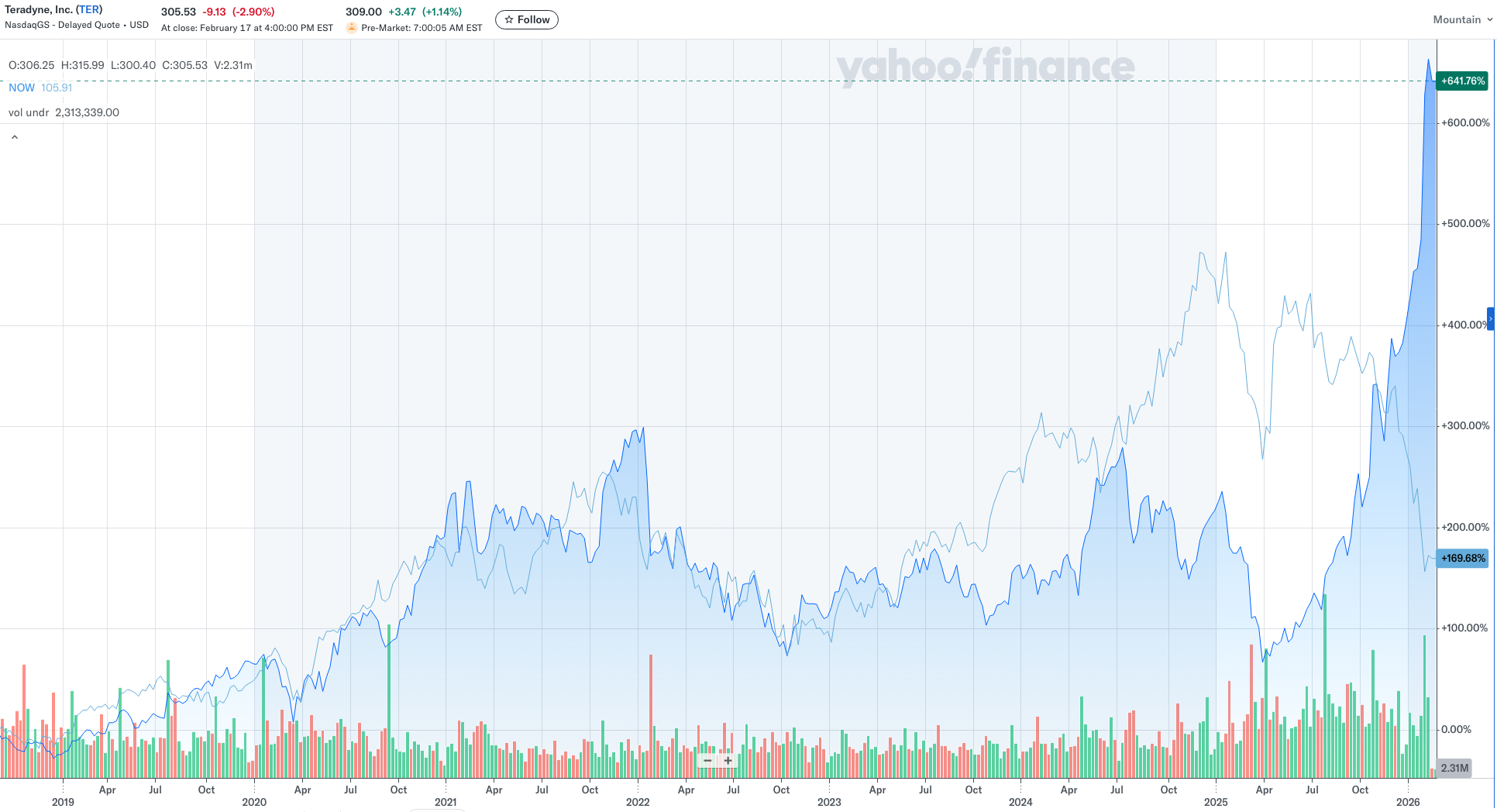

If you were to simply look at a chart that compares the price movement of Teradyne vs ServiceNow you could probably reverse-engineer the latest narrative to emerge and even pinpoint when it really caught hold.

These two charts were highly correlated for years until at first a narrative emerged in late 2024 that SaaS would be a major beneficiary by integrating automation and agents into their products, which propelled NOW way ahead of TER.

But then a rethink occurred in mid-2025 where the market began to question whether traditional SaaS would in fact benefit or just be destroyed entirely. Meanwhile, robotics and automation stocks like TER began to go vertical as the extension of the idea that traditional software would die was that automation and robotics would take over.

If we were to speculate that that narrative has reached a fever pitch with a combination of fear and excitement, we could then try and predict what happens next for this trade.

While I’m not sure I love diving back into software stocks, they do seem to be trying to form a base and I do think perhaps I’m reading fewer people trying to aggressively buy dips. I’m also starting to hear more people suggest SaaS will in fact be disrupted. All signs of possible capitulation on software. I do think this latest narrative has created a lot of confusion for SaaS vendors so their strategies going forward are a huge question mark and I believe will mark a turning point for the industry. As they say, “chaos is a ladder.” So I’m pretty much ambivalent towards software as a group.

However I think the bet against automation consuming everything is a good one at least in the short term. I believe a sort of mini bubble may have emerged here where the narrative has vastly outpaced the fundamentals and I’m not sure how much further that narrative can be extrapolated without some evidence of its truth.

I also think a rethink of that will have much larger implications than just TER stock and will come for semiconductors as well.

Once again the crowd has shown its ability to draw real world narratives from stock prices.

There is very much a precedent here. In 2017 it was none other than ROBO, the automation and robotics ETF of which TER is the largest component, that was ripping to new highs every day while a similar narrative about automation was rippling through markets. Despite the stock market (and speculation) surging, there was daily fear about Amazon killing everything in its path after they acquired Whole Foods in June of that year.

September 22nd, 2017: Amazon Takes Over the World

October 16th, 2017: Just Own the Damn Robots

It’s worth noting that TER went on to surge roughly 40% over three months after these articles were published. AMZN nearly doubled and didn’t finally top until August of 2018. The point is that the end of this illusion was in hailing distance.

Well, a few months into 2018 the spec trade tripped and fell on its face and ROBO fell 35% by the end of the year. This setup feels remarkably similar both in price action as well as narrative. Interestingly, TER has never had a higher RSI on a weekly basis. The odds are stacking in favor of this fading hard.

It’s unclear what exactly would actually cause a rethink but it’s not really important as usually there isn’t a single reason for a selloff, one of the main reasons they are so difficult to navigate.

Trade idea- short ROBO/TER, perhaps short NVDA. I do think this is an early call and the price divergences will likely continue which will reflexively cause more panic around software and further strenghten the narrative that automation is coming for us all but I’d say we are at most a couple months away from this trade reverting to the mean along with the narrative.

2026

- The Nvidia Bear Case

- Thoughts at the quarter mark

- Automation is coming for our jobs once again

- Thoughts as we begin 2026

2025

2022

- A Crash Post Mortem

- What a wild week

- When the facts change...

- Going out on a limb

- No, this is not the late 90's.

- The Crash Isn't Here. Yet.

2021

- This indeed looks like a blow-off top.

- Volmageddon Part II?

- Bear Market Rallies

- Narrative Shifts

- Risk is Rising

- Market Update

- Gauging Sentiment

- Feels Euphoric Out There This Morning

- Markets are Organisms

- Finally, a Decent Setup

- Blow-Off Rallies

- Market Outlook for 2021